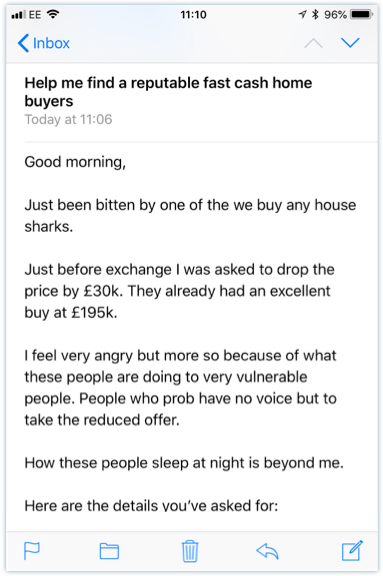

Shady cash buying companies will make an unrealistic high offer and promise to get the money in your hands in a matter of days pending an official valuation.

Using every delay and stall tactic in the book, these companies will drag out the process for months.

At the last possible moment, these companies will cut you back savagely when you’re out of time and unable to do anything other than to accept.

Some companies will also push you to sign paperwork (hoping you don't read the fine print) that prevents you from selling to anyone else.

"The [Quick Sale industry] is yet another area of the property sector where there is no formal regulatory framework.

Whilst I note that the OFT is pursuing a self-regulatory approach, the only way of realistically ensuring all such firms provide consistent service is through legislation."

Asks for an upfront payment of any kind.

Asks for any cancellation or withdraw fee within their paperwork.

Asks you to sign a ‘lock-in contract’, ‘option agreement’ or ‘RX1’ form.

Claims to provide a guaranteed sale for close to 100% of market value.

Claims they (or the industry) are ‘regulated’ by a government body.

Claims they can sell your house to investors for +90% of market value.

Wants to put a 'restriction' against the title of your property with HM Land Registry.

Does not have a clearly visible Company Registration Number on their website.

Cannot provide ‘proof of cash funds’ upon your request.

We regularly mystery shop cash house buying companies that operate in England, Wales and Scotland.

We collect stories from sellers using these companies – this keeps our finger on the pulse of who is (and isn't) providing a fair service.

We verify that companies actually have the cash readily available to buy your home.

An option most sellers don’t know about…

Your answer: Put the best local agents in competition with one another — it’s proven to get you a faster sale and a better price.

The twist: Normally multi-agency costs more and is a hassle to manage. Flyp make it the price of a single agent, and take care of everything.

Reported by the Flyp Marketplace.

“It’s the route I’d point my own family to.”

Gavin Brazg, Founder, TheAdvisory · The Times’s go-to quick-sale expert

Free · no obligation · you’re not committing to anything