Insider Guide:

Conveyancing Fees & Quotes

Don't let hidden costs catch you out

2026 update

Page highlights

- Average conveyancing fees when buying or selling

- The sneaky hidden costs you need to look out for

- The right way to compare quotes

"TheAdvisory drips in honest-to-goodness practical advice for todays house sellers"

Table of Contents

-

The problem you face

-

The truth about fees

-

How much should you expect to pay?

-

When do you pay the fees?

-

What to watch out for when comparing quotes

-

Selling: What should be in the quote

-

Buying: What should be in the quote

-

Look out for these hidden extras

-

The ‘Completion Statement’ explained

-

Fixed fee conveyancing services explained

-

No sale no fee conveyancing services explained

-

Are cheap conveyancing solicitors a false economy?

-

Is the cost of conveyancing increasing?

-

Key Takeaways

-

Related guides

The problem you face

Many conveyancing quotes are out to trick you, so be warned!

Because conveyancing has become such a competitive business, many firms employ tricks to make their conveyancing quotes look cheaper than they actually are.

This is your guide to what costs should (and should not) be included in an online (or off-line) quote.

This information will stop you being ripped-off.

The truth about fees

The key insight to know when shopping for conveyancing is this…

Accurate quotes should have two parts:

Part #1 – The conveyancer’s basic fee

This is the basic cost of your solicitor’s time (and expertise) for processing your transaction.

It can vary a lot between firms (a spread of £500 is not unusual).

For now just keep in mind two points:

- High cost doesn’t automatically equal better service.

- Anything too cheap should ring alarm bells.

Part #2 – Disbursements

Disbursements are are items your conveyancing solicitor will have to pay for on your behalf to third parties and are usually payable irrespective of whether or not your conveyancer offers a ‘no move no fees‘ service.

The cost of each disbursement should be roughly the same from one conveyancing quote to the next…

They are after all, fixed charges and I’ll list them all (along with what they should cost) a little later on.

During the course of the transaction, unavoidable additional disbursements may have to be purchased. Your conveyancer should tell you about any such costs as soon as they come to light.

Total Cost = Conveyancer’s Basic Fee + Disbursements

How much should you expect to pay?

Selling only (<£500k property)

- Expect good conveyancing solicitors to cost £600-£800 if selling a freehold property with a mortgage.

- Add £150-£400 if it’s leasehold

- Subtract £50 if there’s no mortgage.

- A ‘Premier league‘ conveyancing service will cost £1,000 – £2,000 but it’s rarely needed when selling.

Be wary of any service where the ‘conveyancer’s basic fee’ is much less than £500 (freehold sale) or £600 (leasehold sale)

Buying only (<£500k property)

- Expect decent conveyancing to cost £1,000-£1,500 (not including SDLT) if buying a freehold property with a mortgage.

- Add £150-£400 if it’s leasehold.

- Subtract £100 if you’re buying with cash.

- A ‘Premier league‘ conveyancing services will cost £1,500 – £3,000.

- Going ‘Premier league’ is worth considering if buying; new build, leasehold or anything out of the ordinary.

- Conveyancing when buying is all about protecting you from landing up owning a ‘money pit’.

- Good advice doesn’t come cheap so try not to let your choice of conveyancer come down solely to cost.

Be wary of any service where the ‘conveyancer’s basic fee’ is much less than £600 (freehold sale) or £750 (leasehold sale)

When do you pay the fees?

When you instruct a conveyancer or solicitor you will need to send them an ‘upfront payment on account‘.

This is usually £250-£500 but can be a bit more depending on the conveyancer and whether the property is leasehold or unregistered.

This money covers costs to 3rd parties relating to initial disbursements, such as:

- Online ID checking fees

- Searches

- Purchase of official copies from HM Land Registry

- etc..

Your conveyancer having ‘funds on account’ saves time and the ‘faff factor’ of having to request money from you several time throughout the course of your transaction.

Buying: What to expect?

- On instruction you pay £100 – £500 to your conveyancer so they can order your property searches.

- There is then nothing more to pay until you exchange contracts where you typically need to pay 10% of the purchase price (this is not always the case and your conveyancer will advise).

- The balance of the money is paid the day before completion (including stamp duty, land registry free and the balance of your conveyancer’ fees).

Selling: What to expect?

- On instruction you pay £150 – £500 to your conveyancer and then the balance of the money is paid on completion.

- It is common practice for the conveyancing solicitor to take out their conveyancing fees and pay all other disbursements and estate agency fees out of the sale proceeds on completion.

What to watch out for when comparing quotes

A little trick some conveyancing firms like to employ is to invent disbursements.

These firms take tasks and charges that should be covered by the conveyancer’s basic fee – call them; ‘potential additional disbursements’ (or hide them away in small print) and put a hefty price tag on them.

This does three things:

- It sneakily creates extra profit for the conveyancing firm.

- It gives you the impression that their basic fee for doing the work is lower than it really is.

- It turns what initially looks like a cheap conveyancing quote into something far more expensive.

If you come across an ultra-cheap conveyancing quote online (sub-£300), it’s a safe bet to assume this trick is being used to misrepresent the true cost of the service.

There will be a sting in the tail when you receive your final bill at the end of the transaction.

Two rules for comparing quotes accurately

Rule #1 – Be wary of any quote that does not fully itemise all disbursements.

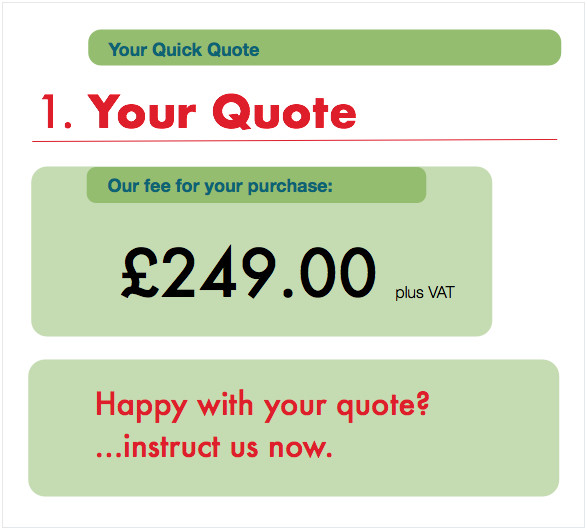

Here’s an example of the type of thing to watch out for:

- Now, this is a fictional example but as you can see, this quote just provides the bare minimum (just the solicitor’s basic fee) and as a result, looks dirt-cheap.

- Many companies quote in this way and make you have to look quite hard to find a link to the detailed cost breakdown of all disbursements.

- Before you instruct them, make sure you find the disbursements and see the full extent of all the costs you’ll be charged.

Rule #2 – Always scour the small print for hidden or unexpected additional charges.

Transparent firms will have just a very short list of fair and reasonable additional charges.

Sneaky firms will have a list as long as your arm where most of the ‘potential’ additional costs should simply already make up part of the conveyancer’s basic fee.

I’ll list all the most common ‘extra charges’ shortly…

It’s impossible for initial quotes to be 100% accurate

Buying: As the conveyancing process progresses, your conveyancer may recommend extra specialist searches in order to fully access the risk of buying the property – These will most likely be unavoidable and unforeseen.

Selling: If you’ve lost important paperwork, your purchaser may insist you buy an indemnity insurance policy to cover their future liability.

Your initial reaction may be of indignation, but many a transaction on the brink of failure has been salvaged because the seller had the good sense to see the cost of an indemnity insurance (usually £100-£200) as small price to pay to get the deal over the line.

Bottom Line

- Most online conveyancing fees calculators do a fairly good job of detailing all the average conveyancing fees that are to be expected.

- That said, there are one or two sites out there that go out of their way to hide disbursements away in the small print to deliberately make their fees seem cheaper than they really are.

- Whatever the online quote estimate may say, you must check the itemised breakdown of fees that will be set out clearly in your conveyancer’s initial ‘client care letter’ (you will receive this at the start of the conveyancing process, before any fees are requested or payable).

Selling: What should be in the quote

SELLING: Typical Conveyancing Quote Breakdown

| Itemised costs to expect: | Typical cost: |

|---|---|

| Conveyancer's basic fee | £300-£1,500 +VAT |

| ID check | £6-£20 +VAT |

| Bank TT fees | £20-£50 +VAT |

| Office copies & Title Plan | £6-£24 (no VAT) |

| Common potential extras: | |

| Mortgaged property supplement | £50-£150 +VAT |

| Leasehold property supplement | £100-£200 +VAT |

| Official copy of Title & Lease | £6-£12 (no VAT) |

Pro Tip: If an online quote is missing items from the list above, consider that quote incomplete.

Contact the conveyancing firm and get clarity on the cost of any missing items so you can get a grip on what the true cost of their service is likely to be.

Standard costs & disbursements

Conveyancer’s Basic Fee (£300 – £1,500) +VAT

- This is the cost of the conveyancer’s time & expertise in processing your transaction.

- You’ll find solicitors & licensed conveyancers tend to charge in 1 of 3 ways:

- On a ‘fixed-fee’ basis (quite rare)

- On a scale that links their fee to the value of the property you’re buying or selling (the most common)

- On a ‘per hour‘ basis (reasonably common)

ID Check (£6 – £20) +VAT

- To meet Money Laundering Regulations your conveyancer must get proof of your identity.

- There is no one way to do this and so the process (and cost) can differ between conveyancing companies.

- For example, some may use 3rd party identity verification services while others will perform online ID checks using Equifax.

Bank TT Fees (£20 – £50) +VAT

- Telegraphic Transfer fees (TT fees) are charged by a bank or building society to send sums of money larger than £60,000.

- Below this amount, the money can be sent for no charge via the Bank Automated Clearing System (BACS).

- If you have a mortgage to redeem then another TT fee will need to be paid.

Land Registry Office / Official Copies (£6 – £24) no VAT

- When your conveyancer prepares the ‘pre contract pack’ to send to the buyer’s conveyancer at the start of the transaction, they must include up to date official copies of the freehold Title Register and filed Title Plan held at HM Land Registry.

- Together these are known as ‘Office Copy Entries’.

- These documents prove the seller owns the property and also detail any ‘Legal Charges’ or ‘Notices’ registered against the title.

Reasonable potential extra costs & disbursements

Mortgaged Property Supplement Fee (£50 – £150) +VAT

- If you have a mortgage, your conveyancer will have additional work liaising with your lender and processing the redemption of your mortgage.

- All this extra work should be reflected in the quote as an increase to their basic fee or as a standalone supplement fee.

Unregistered Property Supplement Fee (£100 – £200) +VAT

- Most properties are ‘registered’ with HM Land Registry, some are not.

- The conveyance of unregistered property requires extra work not least because a physical copy of the title deeds will need to be located or if lost, evidence presented to Land Registry to prove your ownership.

- All this extra work should be reflected in the quote as an increase to their basic fee or as a standalone supplement fee.

Leasehold Property Supplement Fee (£100 – £200) + VAT

- When selling a leasehold property, many conveyancers increase their basic fee to account for leasehold conveyancing being more complicated and time consuming.

- All this extra work should be reflected in the quote as an increase to their basic fee or as a standalone supplement fee.

Official Copies of Title & Lease (£6 – £12) no VAT

- For leasehold properties, official copies of both the leasehold and freehold title must be produced and those relating to any intermediary landlords.

- The official copy of the lease will also need to be retrieved so it can be passed to the buyer.

Managing Agents Pack (£150 – £300) +VAT

- If the property is leasehold the buyer will expect a Managing Agent’s pack to be supplied and paid for by the seller.

- This pack contains information about the property, including service charges, ground rent, major works, company accounts information, etc.

- You won’t often find this cost included in online conveyancing quote breakdowns as the conveyancer has no control over it.

Leasehold Management Information Pack (£150 – £500) +VAT

- If the property is leasehold, you or your conveyancer will need to get this information pack from the freeholder or managing agent.

- These documents will detail things such as the ground rent payable, any service charges, information about upcoming major works which leaseholders will be expected to contribute to and whether leaseholders have applied to purchase the freehold.

- It should also include the management company’s accounts for the last three years.

- You won’t often find this cost included in online conveyancing quote breakdowns as the conveyancer has no control over it.

Indemnity Policies (£20 – £300) +VAT

- Depending on search results and enquires, the buyer may require the seller to purchase an insurance policy to protect them from future liability – e.g. covenant consent hasn’t been sought for the erection of (or alteration to) an out building or there are missing professional installation certificates etc.

- The purchase of any potential policy should be checked with you.

Buying: What should be in the quote

BUYING: Typical Conveyancing Quote Breakdown

| Itemised costs to expect: | Typical cost: |

|---|---|

| Conveyancer's basic fee | £400-£2,000 +VAT |

| Search Pack* | £150-£300 (no VAT) |

| Bank TT fees | £20-£50 +VAT |

| ID check | £6-£25 +VAT |

| Bankruptcy & pre-completion searches | £2-£30 (no VAT) |

| Land Registry fees | Fixed scale |

| Stamp Duty Land Tax | Fixed scale |

| SDLT return fee | £50-£100 +VAT |

| Common potential extras: | |

| Mortgaged property supplement | £100-£300 +VAT |

| Leasehold property supplement | £100-£300 +VAT |

| Lawyer Checker | £10-£15 +VAT |

| Help-To-Buy ISA admin fee | £12 (no VAT) |

| Mining / mineral extraction search | £25-£120 (no VAT) |

| Chancel repair liability search | £20-£90 (no VAT) |

| *The ‘Search Pack’ should (as a minimum) include: 1. Local Authority search 2. Drainage & Water search 3. Environmental search |

|

Pro Tip: If an online quote is missing items from the ‘itemised costs to expect’ list above, consider that quote incomplete.

Contact the conveyancing firm and get clarity on the cost of any missing items so you can get a grip on what the true cost of their service is likely to be.

Standard costs & disbursements

Conveyancer’s Basic Fee (£400 – £1,500) +VAT

- This is the cost of the conveyancer’s time & expertise in processing your transaction.

- You’ll find solicitors & licensed conveyancers tend to charge in 1 of 3 ways:

- On a ‘fixed-fee’ basis (quite rare)

- On a scale that links their fee to the value of the property you’re buying or selling (the most common)

- On a ‘per hour‘ basis (reasonably common)

Search Pack (£180-£300) no VAT

Searches are enquires made on your behalf by your solicitor / licensed conveyancer to various authorities that hold information about your property, the land it sits on or factors that may directly (or indirectly) effect it.

A comprehensive search pack should contain:

- Local Authority search – to check the local land charges register for conservation areas, tree preservation orders, listed building designations, improvement or renovation grants, smoke control zones, & future developments. It also investigates; building control history, planning control history, nearby road schemes and motorways, contaminated land and radon gas.

- Drainage & Water search – this checks locations of drains and sewers, how water drains away and if the property is connected to the mains water supply.

- Environmental search – this primarily investigate the risk of land contamination.

Dependent on the area in which you are purchasing your property, other recommended searches may be required, but this will be advised at the point of instruction by your conveyancer.

The most common additional searches are:

- Location specific mining searches (£25-£120) – if you live an area of historic coal, tin, limestone, China clay or Cheshire brine mining, these searches will discover when workings ceased and if subsidence has been an issue.

- Chancel Repair Liability search (£20-£90) – to find out if you are expected to contribute to the upkeep of the parish church; a cost which could run into tens of thousands.

Bank TT Fees (£20 – £50) +VAT

- Telegraphic Transfer fees (TT fees) are charged by a bank or building society to send sums of money larger than £60,000.

ID Check (£6 – £25) +VAT

- To meet Money Laundering Regulations your conveyancer must get proof of your identity.

- There is no one way to do this and so the process (and cost) can differ between conveyancing companies.

- For example, some may use 3rd party identity verification services while others will perform online ID checks using Equifax.

Stamp Duty Land Tax (fixed rates) no VAT

- This is a transfer tax paid to the government by the buyer of a home or land in England, Wales and Northern Ireland.

- If you purchase property or land in Scotland, you pay Land and Buildings Transactions Tax (LBTT) instead.

- Most online quotes automatically workout how much SDLT you’ll have to pay however, some cheeky quotes don’t include the stamp duty (and as such can look phenomenally cheap).

- SDLT works like income tax in that you pay the required rates on the amounts which fall into each band.

The current standard rates are:

Stamp Duty Land Tax Rates

| brackets | rates |

|---|---|

| Up to £250,000 | 0% |

| The portion from £250,001-£925,000 | 5% |

| The portion from £925,001-£1.5m | 10% |

| The portion above £1.5m+ | 12% |

| source: GOV.UK |

- If the property you are purchasing counts as an ‘additional’ residence (i.e. if you already own or part-own a property) you will pay an additional 3% on the whole price.

- This maybe refundable if you are selling your home at some stage within the next 36 months.

- Stamp duty is payable to HMRC within 30 days of completion but funds will be required by your conveyancer or solicitor before you can complete.

More: Stamp duty land tax explained

Filling out the Stamp Duty Tax Return (£20-£50) +VAT

- In 2003 the tax form went from being a single page document to having seven pages. Some conveyancers include this work within their basic fee, others list it as a separate cost.

- Where it should not be is hidden away in the small print.

- Given most purchases are liable for SDLT, you need to know if your conveyancer is going to charge you extra or not.

Bankruptcy and pre-completion searches (£2-£30) no VAT

- These searches are made after exchange of contracts to make sure nothing has changed with regard to the property or your ability to purchase the property.

Land Registry Fees (£20-£455) no VAT

- This is a payment to HM Land Registry for updating the records they hold about the property your buying and to register you as the new owner.

- The cost of this depends on the price of the property you’re buying.

- There is a set fee scale and most instant quotes should work this out for you.

For reference, the basic set fee scale is:

HM Land Registry Fees

| Price paid for your property: | Fee to pay: |

|---|---|

| 0 to £80,000 | £20 |

| £80,0001 to £100,000 | £40 |

| £100,001 to £200,000 | £95 |

| £200,001 to £500,000 | £135 |

| £500,001 to £1,000,000 | £270 |

| £1,000,001 and over | £455 |

| source: HM Land Registry | |

Reasonable potential extra costs & disbursements

Mortgaged Property Supplement Fee (£100 – £300) +VAT

- If you’re buying with a mortgage, your conveyancer will have additional work liaising with your lender.

- All this extra work should be reflected in the quote as an increase to their basic fee or as a standalone supplement fee.

Leasehold Property Supplement Fee (£100 – £200) + VAT

- Buying a leasehold property is more complicated and makes more work for conveyancers.

- All this extra work should be reflected in the quote as an increase to their basic fee or as a standalone supplement fee.

Help-to-Buy Supplement fee (£200 – £350) + VAT

- If you are taking out an equity loan there will be more work for your conveyancer.

- Many online quotes have the facility for you to flag this and have it itemised as an additional disbursement or added to the conveyancer’s basic fee.

Help-to-Buy ISA fee (£12 – £50) no VAT

- This is a statutory fee only chargeable if you have a Help-to-Buy ISA that requires your conveyancer to obtain the bonus from the scheme.

- Many online quotes have the facility for you to flag this and have it itemised as an additional disbursement or added to the conveyancer’s basic fee.

Landlord / managing agents fee (unknown)

- When buying a leasehold property, your conveyancer will need to deal with your landlord and/or management company following completion to deal with the change of ownership.

- The management company will likely charge to deal with the administration of this and any other requirements under the lease.

Lawyer Checker (£10-£15) +VAT

- If the conveyancer acting for the seller is unknown to your conveyancer, they will complete a lawyer checker search to confirm details of the conveyancer and prevent the risk of fraud.

- Not all conveyancers do this as standard so check as the risk of fraud is real (and growing).

Reasonable additional costs in exceptional circumstances

This is not a definitive list, but covers the main exceptional costs you may encounter:

Exceptional Additional Conveyancing Costs

| Item: | Typical cost: |

|---|---|

| Corresponding and collecting in funds from third parties | £80-£150 plus VAT |

| Unregistered title for freehold | £80-£150 plus VAT |

| Unregistered title for leasehold | £80-£150 plus VAT |

| Deed of Covenant | £125-£200 plus VAT |

| Arranging an indemnity policy | £80-£120 plus VAT |

| Exchange deadline required within 21 working days or receipt of contract | £100-£200 plus VAT |

| Completion deadline required within 21 working days of receipt of contract | £100-£200 plus VAT |

| Completion within 5 working days of exchange of contracts | £100-£200 plus VAT |

| Discharge of an individual mortgage (other than repayment of the first mortgage) or other entry of a financial nature | £95-£150 plus VAT |

| Dealing with Defective Titles | £50-£100 plus VAT |

| Where a Guarantor is involved | £150-£300 plus VAT |

| Dealing with Contaminated Land issues | £95-£150 plus VAT |

| Dealing with two titles | £50-£80 plus VAT |

| Purchasing a share of freehold title in conjunction with leasehold title | £95-£150 plus VAT |

| Dealing with Certificate of Compliance for either freehold or leasehold property | £95-£150 plus VAT |

| Dealing with solar panel documentation | £100-£150 plus VAT |

| Dealing with private drainage | £75-£150 plus VAT |

| Dealing with Building Regulation Enforcement Notice | £50-£100 plus VAT |

| Dealing with underpinning or structural matters | £100-£200 plus VAT |

| Dealing with Standard Statutory Declaration | £75-£150 plus VAT |

| Reviewing existing Assured Shorthold Tenancy Agreement on purchase | £75-£150 plus VAT |

| Dealing with and Administering retentions | £50-£100 plus VAT |

| Dealing with HMLR ID1 forms | £50-£100 plus VAT |

| Dealing with Restrictions on Register with HMLR | £75-£300 plus VAT |

| Dealing with certificate of Bankruptcy registered as any entry on title | £50-£100 plus VAT |

| Dealing with HMO (Houses in Multiple Occupation) | £75-£150 plus VAT |

| Dealing with porting requirement from existing to new mortgages | £95-£150 plus VAT |

Look out for these hidden extras

Below are costs (you’ll almost certainly have to pay) that often get hidden away or called ‘potential additional costs’.

…There ain’t nothing ‘potential’ about them!

When comparing quotes, make sure the cost of these items have been accounted for.

That way you’ll be making a true ‘like for like‘ comparison and protect yourself from getting a big shock when your final bill arrives.

PI Contribution (£50 – £100) +VAT

- ‘PI’ stands for ‘Professional Indemnity’ and it’s a particularly odious little charge.

- Basically the firm is trying it on and it should already be included as part of the conveyancing solicitor’s basic fee!

- Don’t use a firm that tries this trick with you. It’s an overhead of their business and they have no right asking you to make a contribution.

Postage, Photocopying & Phone Calls (£5 – £50) +VAT

- These are overheads of business and should be covered by the conveyancer’s basic fee, not listed in the small print as a potential additional cost.

- International phone calls & postage maybe, but only if they are fully itemised!?

SDLT Return Filing Fee (£20 – £50) +VAT

- Not only does your SDLT return need to be filled in, it also need to be submitted to HMRC.

- Even if you’re under the SDLT threshold, a SDLT return will need to be filed with HMRC.

- As such, this is a cost you’re going to incur (unless you fancy filing the SDLT return yourself).

Archiving / File Storage Fee – (£15 – £50) + VAT

- Following completion your conveyancer should hold onto your file documents for a number of years.

- Most conveyancers store client’s documents as standard but some charge extra.

- You will want to pay for this because you may well need to dig into the file if problems post-completion come to light.

The ‘Completion Statement’ explained

When buying:

- The completion statement is basically ‘the bill’ for your property purchase.

- It’s a document given to you by your Solicitor/Licensed Conveyancer, which details all the payments you’ve made (and need to pay) to them throughout your transaction (including their conveyancing fees).

- A draft completion statement is sent to you upon your conveyancer’s receipt of your mortgage offer or if buying with cash, before exchange of contracts when requesting deposit monies.

- A further second draft is sent between exchange and completion and a final is sent on completion.

- Everything in the completion statement has to be paid and cleared with the bank before the completion deadline in order for a purchase to go through.

- Your conveyancer will also send you a separate document for your reference that fully breaks down how the conveyancing fees portion of the completion statement has been calculated.

When selling:

- On completion of your sale, your conveyancer will send you final statement that details all the deductions that have come off the sale proceeds prior to the final balance being transferred to you.

- The typical deductions are: estate agent’s fee, conveyancer’s fee & disbursements.

How do I complain about my solicitor charging extra fees?

Most people are happy with their conveyancer – according to The Legal Services Consumer Panel’s Tracker Survey 2017, 93% of consumers who use legal services for conveyancing are satisfied.

But problems can occur so read your completion statement carefully and query any charges you do not understand. It may be that your conveyancing provider can clear up any confusion.

That said…

If you think you’ve been overcharged and want to make a formal complaint, do this:

step 1: Write to your legal company to explain what action you would like them to take.

step 2: If this does not resolve the issue, you must follow the firm’s official in-house complaints procedure (details of which should have been given to you when you first instructed them. If it wasn’t, it will be available on request).

step 3: If after 8 weeks you’re not had a satisfactory response and a resolution cannot be reached, you may take your complaint to the Legal Ombudsman.

More: How to make complaints & resolve problems with conveyancers

Fixed fee conveyancing services explained

Fixed fee conveyancing solicitors offer a service at a ‘fixed’ price – which means the price quoted at the outset will be the price you pay for their legal services and any disbursements included.

How do they work?

- It is important to note that fixed fee deals are not the same for everyone, so if a friend has recommended a fixed fee conveyancer or solicitor to you, you will not automatically pay the same price they will.

- ‘Fixed’ typically relates to the price of the legal services provided, not all of the third party legal costs incurred during the process.

- The fixed element of the quote does not include disbursements, although these should be included in the quote, as the need for further searches may arise.

Pros & Cons (and misleading claims)

Pros

It gives you the opportunity to budget more accurately for your legal costs with, theoretically at least, no hidden charges and surprises.

Cons

Unclear communication can cause misunderstandings over costs, so:

- Give the solicitor/conveyancer all the information you have about the transaction so they can prepare an accurate quote. Tell them if the property is leasehold, Shared Ownership, involves a Help to Buy deal etc.

- Read the small print carefully to check for hidden charges and the potential for rising costs.

- Query anything you costs you don’t understand and ask for clarification over how much the final cost will be.

The rise of fixed price conveyancing

In the past, most people used their local solicitor to carry out property conveyancing, paying by the hour. But this has the disadvantage that costs can soon spiral out of control.

In recent years there has been a trend towards the ‘fixed fee’ model, with more and more licensed conveyancers in particular offering fixed fee deals; 70% in 2016, rising to 73% in 2017, according to The Legal Services Consumer Panel [1].

The rise in internet use also means consumers can shop around and an access the services of a wider range of businesses, although fewer people do so than you might expect.

The Legal Services Consumer Panel’s Tracker Survey 2017 reports:

- Overall, only 27% of people shop around for legal services (not just conveyancing)

- 79% of consumers say they have a fair or great deal of choice when it comes to conveyancing

- 51% of consumers use email or the internet during the conveyancing process

- Of those who use a solicitor, 76% choose a local company

New rules, which allow non-lawyers to manage law firms, mean fixed fee conveyancing and internet-only businesses are increasing, and estate agencies and mortgage brokers are able to move into the residential conveyancing market, too.

Very large online firms are often referred to as ‘conveyancing factories’, and it is feared that some of these put volume of business over customer service, particularly where a transaction is anything other than straightforward [2].

No sale no fee conveyancing services explained

A ‘no sale, no fee’ or ‘no move, no fee’ service is worth looking out for…

But bear in mind, its not strictly accurate to think you won’t pay a penny to your solicitor or conveyancer if your property transaction falls through.

It’s just the conveyancer’s basic fee for their time spent dealing with our case that you get let off.

You’ll still get a bill for any payments your conveyancer has made on your behalf to 3rd parties, such as; search providers, managing agents or the Land Registry etc.

Pros & Cons

Pros

- If the purchase or sale falls through – often due to factors outside your control – you will not have to pay the legal fees

- Your legal representative should have a good incentive to keep things moving – as, if the sale falls through, they will not get paid for their time.

Cons

- There is no such thing as a free lunch, so the cost of a no sale, no fee package may be slightly higher to compensate the legal company for all those sales, which fall through.

- Some less than scrupulous companies hide additional ‘disbursements’ in the small print, so you still end up paying them for things which should be considered normal overheads, such as postage, telephone calls and photocopies.

Are cheap conveyancing solicitors a false economy?

Buying a property is a major purchase with the potential for massive financial lose and aggravation.

You need a conveyancer who looks for solutions not problems and one, which is proactive, not ‘reactive’.

When budgets are tight, it can be tempting to cut corners where you can, but cheap conveyancing is rarely a good idea:

- Companies can only offer cheap deals by taking on huge volumes of cases – which means they will struggle to give yours the attention it needs, slowing down your transaction.

- They are likely to be stalled by problems, putting your case to the bottom of the pile while they clear the ‘easier’ transactions, which need to complete or exchange that week.

- Cheap conveyancing is usually offered by large conveyancing factories – you may struggle to speak to the same person twice and are unlikely to be given a named contact with a direct number or email address.

- The cheap price they quote is rarely the price you’ll pay as there will most likely be additional costs or the word ‘estimate’ hidden in the small print.

- Without careful focus on your case, things can be missed which cost you in the long run.

Recap: What should you expect to pay?

Selling only (<£500k property)

- Expect decent conveyancing to cost £600-£800 if selling a freehold property with a mortgage.

- Add £150-£400 if it’s leasehold

- Subtract £50 if there’s no mortgage.

- A ‘Premier league‘ conveyancing service will cost £1,000 – £2,000 but it’s rarely needed when selling.

Be wary of any service where the ‘conveyancer’s basic fee’ is much less than £500 (freehold sale) or £600 (leasehold sale)

Buying only (<£500k property)

- Expect decent conveyancing to cost £1,000-£1,500 (not including SDLT) if buying a freehold property with a mortgage.

- Add £150-£400 if it’s leasehold.

- Subtract £100 if you’re buying with cash.

- A ‘Premier league‘ conveyancing services will cost £2,000 – £3,000.

- Going ‘Premier league’ is worth considering if buying; new build, leasehold or anything out of the ordinary.

- Conveyancing when buying is all about protecting you from landing up owning a ‘money pit’.

- Good advice doesn’t come cheap so try not to let your choice of conveyancer come down solely to cost.

Be wary of any service where the ‘conveyancer’s basic fee’ is much less than £600 (freehold sale) or £750 (leasehold sale)

Is the cost of conveyancing increasing?

Yes.

But, according to The Law Society, fees have risen slower than those charged by estate agents and surveyors [3]:

- Conveyancing cost an average of £1,419 in 2014, an increase of 37% on 2004, when the average was £1,039.

- As a percentage of overall costs, conveyancing went down – in 2004 it represented 14% of moving costs, but in 2014 it was 12%.

- In the same period, estate agent fees rose by 61% and surveyors’ fees rose by 51%, and both rose slightly as a percentage of overall moving costs.

Despite the price increases, a growing number of consumers feel they get value for money from their conveyancing services; 62% in 2017 compared with 55% in 2016 [4].

Key Takeaways

#1. Comparing conveyancing quotes can be a tricky business.

- Always check the small print and always calculate the real total price when comparing one quote against another.

- Be wary of cheap headline prices because if it looks too good to be true, it usually is.

#2. Don’t be shy coming forward

- When seeking quotes, give the conveyancing firm all the information you have about the property to avoid any surprise charges when your final bill arrives.

- Leasehold, mortgaged, help to buy, shared ownership are all issues you must alert the conveyancer to.

#3. Disbursements are never free

If your sale falls through you will still be charged for any searches, Office Copy Entries, etc., that have already been ordered and paid for.

#4. It’s unwise to choose your conveyancer based on cost

- Conveyancing mistakes can and do happen.

- When they do, they will cost you dearly both financially and emotionally (and take a long time to resolve).

- Using a cheap service increases the risk of mistakes being made with your transaction.

Related guides

- What is conveyancing?

- Selling: Conveyancing process explained

- Buying: Conveyancing process explained

- DIY conveyancing

- Choosing conveyancing solicitors

- Dealing with conveyancing complaints & problems

- Exchange and completion of contracts explained

- Conveyancing searches explained

- Step by step guide to extending your lease

- Stamp duty land tax (SDLT) explained

Sources, citations and credits

Related guides

Did you

know?..

The hotter your market

the easier your sale...